Updated

• 7 min read (EN)

McKinsey 7-S Framework Explained: 7 Levers and Limits

The McKinsey 7-S Framework is a seven-element model that checks whether a company's strategy, structure, and culture line up well enough to execute. It was built at McKinsey in the late 1970s and formalized in a 1980 Business Horizons article by Robert Waterman, Tom Peters, and Julien Phillips. The premise: a great strategy goes nowhere if any one of the other six elements drifts out of alignment.

Why Alignment Beats Strategy on Its Own

Most investors focus on what a company says it will do. The 7-S idea is that strategy is one piece of seven, and the other six decide whether the strategy ships. Tom Peters' brief at McKinsey came from a simple observation: clever strategies kept failing in execution. The seven levers explain why.

For a stock investor, alignment matters because earnings translate strategy into cash. If structure, systems, or staff cannot carry the strategy, the cash never shows up. Misalignment is the hidden reason long-range plans slip and guidance gets cut. The 7-S gives you a checklist for that hidden reason. Costco's procurement edge, for example, only works because every other element is built around it: a flat structure, a frugal style, and employee retention well above retail norms.

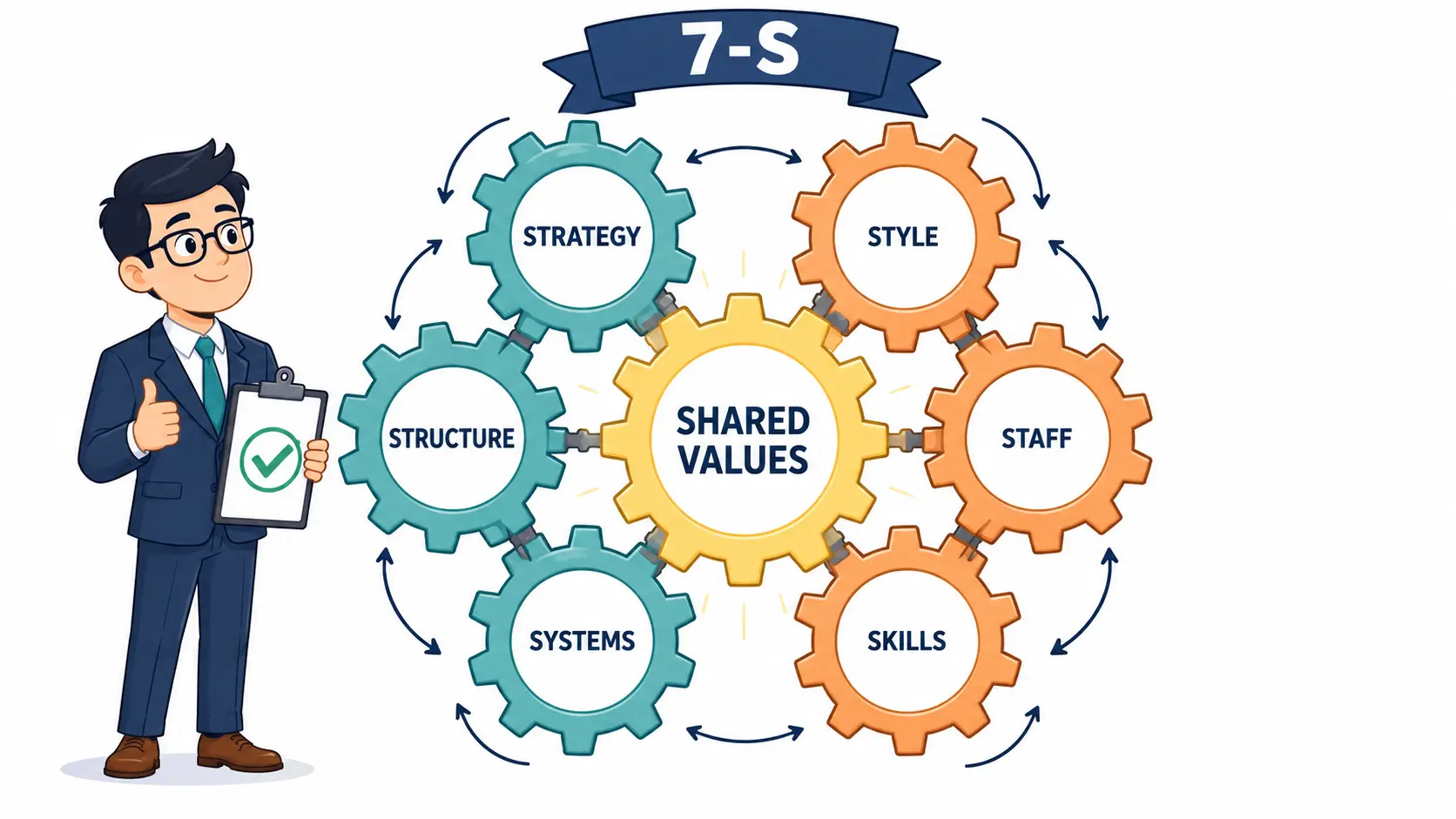

The Seven Elements, One by One

The seven split into three hard levers and four soft levers, with shared values at the center.

Strategy. The plan to win in the market: pricing, positioning, what the company says no to. This is what most analysts focus on by default.

Structure. Reporting lines and how decision rights are distributed: flat, hierarchical, divisional, matrix. A new strategy run through the old structure rarely lands.

Systems. The processes that run the business day to day: budgeting, hiring, supply chain, IT. Systems are where strategy is either enforced or quietly ignored.

Shared values. The unwritten beliefs that explain what gets praised and what gets fired. The 1980 article called this layer "superordinate goals." Anthony Athos renamed it "shared values" in workshop so all seven elements began with S.

Style. How leaders behave: where they spend their time, what they tolerate, what they cut. The signal is sharpest in founder-led companies, where one person's style stamps the whole organization.

Staff. Who the company hires, retains, and promotes, and what its bench looks like. This is one of the cheaper forward indicators in any 10-K appendix.

Skills. The capabilities the company is known for. ASML's lithography expertise is a skill. The procurement engine behind a wide-moat retailer is a skill.

The seven are interconnected by design. Change strategy without changing systems and the new strategy starves. Change structure without changing style and middle managers route around the new boxes.

Hard vs Soft Elements: Why Soft Wins

Strategy, structure, and systems are the hard elements. They live in slide decks and org charts. Investors can read them off a 10-K, an investor day, or a press release.

Shared values, style, staff, and skills are soft. They live in how a meeting runs, how a layoff gets handled, how a promotion gets decided. Soft elements take longer to build, longer to break, and almost never show up in disclosures.

This is why the 7-S slants toward soft elements as the source of durable advantage. A competitor can copy a strategy in a quarter and a structure in a year. Copying a 30-year culture takes a generation. Buffett's preference for businesses that "an idiot could run" is partly a 7-S statement: the soft elements have to be strong enough that ordinary management cannot break them.

Aligned, Misaligned, and Mid-Merger Companies Compared

The same seven elements look different depending on where a company sits in its lifecycle. The table below maps three patterns an investor regularly runs into.

| Dimension | Aligned Compounder | Misaligned Legacy | Mid-Merger Acquirer |

|---|---|---|---|

| Strategy | Clear, narrow focus | Drifted, multi-bet | Two strategies in one box |

| Structure | Flat, fast decisions | Heavy hierarchy | Duplicated functions |

| Shared values | Lived daily by staff | Plaque on the wall | Two cultures clashing |

| Investor signal | Margin expansion | Earnings miss risk | Integration headwinds |

| Best for | Long compounder thesis | Activist target | Wait 2-3 quarters |

The misaligned legacy column is where activists cluster. They take a stake, push for a strategy refocus, sometimes a structure change, and ride the realignment. The mid-merger column is why post-deal stocks often go sideways for several quarters: even a strong combination has to wait for systems, staff, and style to converge. An earnings report walkthrough gives the surface read; the 7-S tells you whether the surface is supported.

Where the 7-S Framework Falls Short

The model has well-known limits, and treating it as a complete tool is a mistake.

It is internal-only. The seven elements say nothing about competition, regulation, or market structure. A perfectly aligned company in a dying industry stays a dying company. Pair the 7-S with an external lens like Porter's five forces if you want a fuller picture.

It does not prioritize. All seven look equal in the diagram, but in practice shared values and strategy carry more weight than the others. The framework does not tell you which lever to pull first.

It is a snapshot, not a movie. The model assumes a relatively stable company. In a fast-moving industry the seven elements drift faster than the analyst can map them.

The framework also took reputational damage from its original showcase. Peters and Waterman applied the 7-S to 43 Fortune 500 companies in In Search of Excellence (1982). Roughly a third of those "excellent" firms hit serious trouble within a few years, including Atari. Bain dinged the framework for "lack of quantitative underpinnings" and looseness of definition. The 7-S is a structured conversation, not a measurable scorecard.

Treat the 7-S as one input. Combine the alignment read with hard fundamentals to see whether the company you like on paper has the organization to deliver.

Frequently Asked Questions

Who created the McKinsey 7-S Framework and when? The framework came out of work at McKinsey in the late 1970s and was formalized in a 1980 Business Horizons article called "Structure Is Not Organization." The named authors were Robert Waterman, Tom Peters, and Julien Phillips, with conceptual help from academics Anthony Athos and Richard Pascale during a two-day workshop in San Francisco. It reached a wider audience through the 1982 book In Search of Excellence.

What are the seven elements of the McKinsey 7-S Framework? The seven are Strategy, Structure, Systems (the three hard elements) and Shared Values, Style, Staff, Skills (the four soft elements). Shared Values sits at the center because it shapes the other six. The model says all seven need to reinforce each other for a company to execute well.

How is the McKinsey 7-S Framework different from a SWOT analysis? SWOT is an external-and-internal scan that lists strengths, weaknesses, opportunities, and threats. The 7-S is internal only and asks whether the existing pieces of the company line up. SWOT asks if the strategy makes sense given the market; the 7-S asks if the organization is built to deliver the strategy. Most analysts use them together.

Can investors use the McKinsey 7-S Framework to evaluate stocks? Yes, but as one input rather than the primary tool. The 7-S highlights organizational alignment risks that fundamentals miss, such as a strategy the structure cannot support or a culture that contradicts the stated direction. It is most useful for long-horizon positions where execution quality is the swing factor: compounders, post-merger acquirers, and turnarounds.