Updated

• 8 min read (EN)

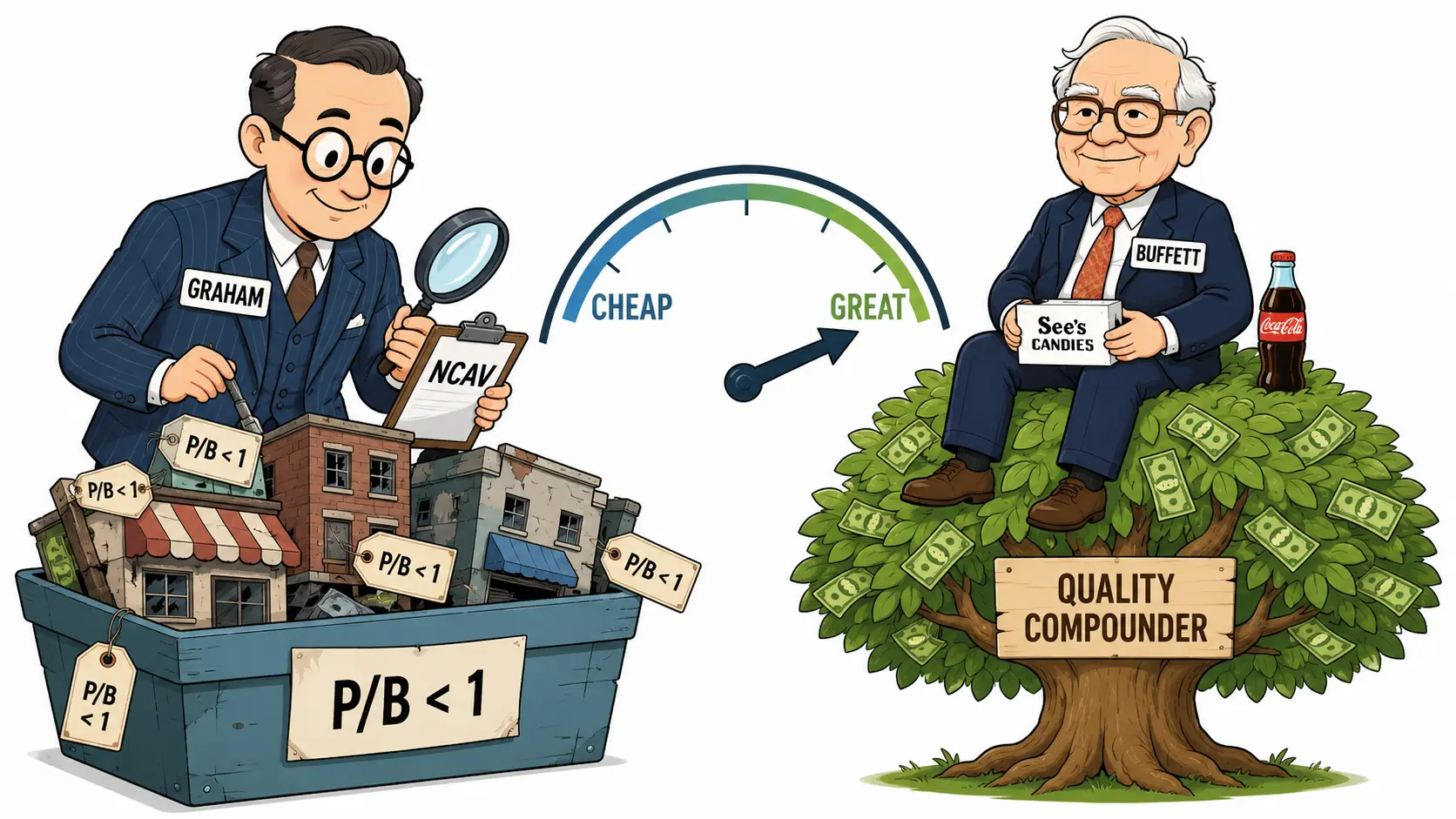

Graham vs Buffett: Deep Value vs Quality Compounders

The split is simple. Benjamin Graham bought statistically cheap stocks and sold them once price caught up to value. Warren Buffett, after Charlie Munger's nudge, started buying high-quality companies at fair prices and held them for decades. Both methods still go by the name "value investing"; the playbooks barely overlap. Run the same stock through the DCF calculator and you can price it through both lenses at once.

Graham vs Buffett at a Glance

Quick comparison before the detail.

| Dimension | Graham (Deep Value) | Buffett (Quality Compounders) |

|---|---|---|

| Goal | Buy at a discount to net asset value | Buy great businesses at fair prices |

| Signature metric | Net current asset value (NCAV) | Return on capital + durable moat |

| Holding period | Until price meets intrinsic value | Forever, in the ideal case |

| Diversification | Wide; 30 to 100+ positions | Concentrated; ~5 names hold 75% |

| Industry view | Sector-agnostic, often micro-cap | Brands, networks, franchises |

| Margin of safety | Quantitative gap to book value | Qualitative durability of cash flow |

| Best for | Bear markets, small AUM | Long compounding at any size |

The Graham column rewards waiting for prices to fall below tangible value. The Buffett column rewards waiting for great businesses to trade at fair prices, then doing nothing.

What Graham's Method Tells You

Graham's approach starts with the balance sheet. He looked for stocks trading below net current asset value: current assets minus total liabilities. He bought at roughly two-thirds of that figure, so the assets covered the price even if the business unwound. His other anchor is Mr. Market, the manic-depressive partner who quotes a different price every day; the investor's job is to ignore the mood and trade only when the price drops far enough below intrinsic value to give a margin of safety. Graham summed it up in The Intelligent Investor, where he called margin of safety "the central concept of investment." The Graham-Newman partnership returned roughly 20% annually from 1926 to 1956 running this playbook.

The blind spot is fit. Graham's screen catches statistical bargains regardless of business quality, so the basket is heavy with value traps where the cheapness reflects real decline. The only catalyst is price reverting to value. A 1986 study of net-net stocks from 1971 to 1983 showed annualized returns of 33.7% versus 12.1% for the benchmark, but the screen now produces almost no candidates in modern bull markets, and most survivors are very small companies.

What Buffett's Method Tells You

Buffett started as a pure Graham disciple and ran his early partnership on cigar-butt stocks, named for the "one puff" of profit they offered. Munger pushed him toward quality. The 1972 acquisition of See's Candies, bought for $25 million at three times book value, was the test case. Buffett and Munger discovered that See's could raise prices every year without losing customers, and the pricing power produced far more cash year after year than the 1972 price suggested. Buffett later said Berkshire would not have bought Coca-Cola in 1988 without the See's lesson on durable brands.

The modern Buffett method buys high-return businesses with wide moats (brands, networks, low-cost production), at fair rather than cheap prices, and holds them while reinvested earnings compound. The Coca-Cola stake bought in 1988 for $1.02 billion was worth $11.6 billion by 1999. The blind spot is overpaying for durability that does not last: when a moat cracks, the multiple unwinds and the long holding period turns against the investor. The Apple thesis only landed in 2016 because the company finally looked durable enough, as the Apple versus BlackBerry hindsight makes clear.

When to Use Graham's vs Buffett's Approach

| Scenario | Graham (Deep Value) | Buffett (Quality Compounders) |

|---|---|---|

| Bear markets | Best fit; bargains everywhere | Wait for moats to go on sale |

| Bull markets | Few candidates pass the screen | Hold; do not chase |

| Account size | Works at small AUM | Scales to billions |

| Time available | Many positions, low conviction | Few positions, deep research |

| Industries | Sector-agnostic, micro-cap heavy | Brands, franchises, networks |

| Best for | Patient screeners with cash | Long-horizon compounding investors |

Use Graham when screening produces enough candidates: bear markets, out-of-favor sectors, or a small enough AUM that micro caps fit. Walter Schloss ran a Graham-style book with more than 100 positions and beat the market for decades by spreading risk thin. The method also fits investors who prefer many small bets to a few large ones.

Use Buffett when patience pays more than turnover. The method needs an investor who can wait years for a great business at a fair price, then sit on the position while cash flow compounds. It also scales: Berkshire holds 47 stocks today with 75% of the portfolio in five names. The same five-name concentration would be reckless in Graham's universe of statistically cheap micro caps.

Using Graham and Buffett Together

The two methods complement each other more than they compete. Graham's screen catches cheapness; Buffett's filter strips out the names that are cheap because the business is dying. A practical synthesis: start with a quantitative cheapness check (P/E, P/B, FCF yield) to narrow the universe, then apply a quality check (return on capital, brand strength, profit margin trend) to keep only the names worth holding. The price discipline is Graham; the holding period is Buffett. Bruce Greenwald's Columbia course from the 1990s onward taught this exact synthesis, and most great value managers now sit somewhere between the two poles. The same logic explains why a growth versus value framing often misses the point: a great compounder is both, depending on the price you pay.

Treat Graham and Buffett as two settings of one dial. Graham gets you in cheap; Buffett keeps you in long. For the price half of the dial, the DCF calculator shows what a stock is worth on cash flow alone; deciding whether the business is also worth owning forever is on you.

Frequently Asked Questions

What did Charlie Munger change about Buffett's approach? Munger pushed Buffett away from buying mediocre businesses at very cheap prices ("cigar butts") toward buying high-quality businesses at fair prices and holding them. The 1972 See's Candies purchase, where Munger talked Buffett into paying three times book value, was the test case. Once Buffett saw that See's could raise prices every year without losing customers, he applied the same lens to Coca-Cola, American Express, and eventually Apple.

Are net-net stocks still findable today? They exist but are rare in large-cap markets. Most modern net-nets sit in micro-cap or small-cap stocks, often outside the United States, and the strategy works only at a relatively small portfolio size. Backtests still show 20% to 33% annualized returns in some periods, but the practical issue is finding enough names to fill a diversified portfolio.

How concentrated is Berkshire Hathaway's portfolio compared to Graham's? Berkshire currently holds about 47 stocks but roughly 75% of the value sits in just five names. Graham-style investors like Walter Schloss have run portfolios with more than 100 holdings, deliberately diluting any single company's risk. The two represent opposite ends of the diversification spectrum within value investing.

Which approach is better for an individual investor today? Neither is strictly better. Graham's method works at small account sizes, in bear markets, and for investors comfortable holding many micro-cap positions. Buffett's method works at any size but requires the patience to hold a great business through multiple cycles and the discipline to skip expensive years. Most modern value managers blend the two: Graham-style cheapness as a screen, Buffett-style quality as a filter.