Published

• 8 min read (EN)

Stock Splits Explained: Ratios, Math, and Why They Happen

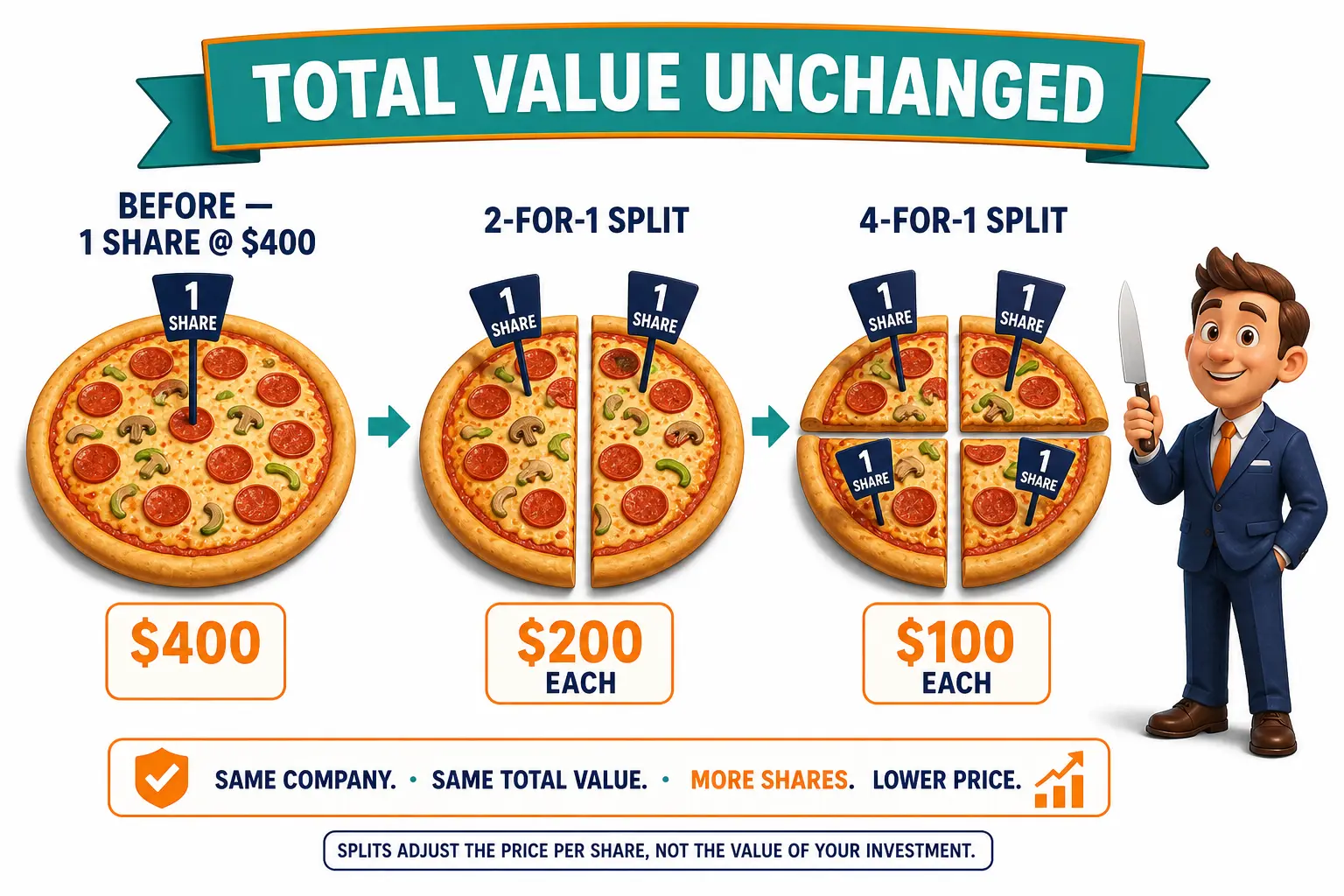

A stock split is a corporate action that changes the number of shares outstanding without changing the company's market cap. The price per share moves in proportion: a 2-for-1 split halves the price and doubles the share count.

Apple, Nvidia, and Tesla have all used splits to make their stock look more accessible without changing what investors own. The math is the same in every case: same pie, more slices.

Why Stock Splits Matter

The company is worth the same the second after the split as it was the second before. What changes is the price tag, the share count, and sometimes the type of buyer the stock attracts.

Three reasons come up over and over.

Make the price look retail-friendly. Before fractional shares became common, a $1,200 stock priced out small accounts. Nvidia split 10-for-1 in June 2024, taking NVDA from roughly $1,200 to $120 overnight. The market cap stayed near $3 trillion. Tesla did a 5-for-1 in 2020 when shares were near $2,200, then a 3-for-1 in 2022.

Stay eligible for the Dow Jones Industrial Average. The Dow is price-weighted, so a $400 stock has 4x the index weight of a $100 stock at the same share count. Apple's 7-for-1 split in 2014 cleared the way for AAPL to enter the Dow in March 2015 without dominating the index. Without the split, a $700 share would have been the heaviest component by a wide margin.

Send a confidence signal. A board only authorizes a forward split when management expects the price to keep climbing. Bank of America's 2024 review of US splits since 1980 found announcing companies outperformed the S&P 500 by roughly 25% in the year after the announcement, though results vary by sample and era. The split itself is not the cause: it is a marker for businesses already firing on all cylinders.

A split does not move the underlying business. It only changes how the share is packaged.

How Stock Splits Work

Two directions exist: forward splits and reverse splits. Both follow the same arithmetic.

A forward split increases the share count and reduces the price. The ratio is announced as "X-for-1," where one old share becomes X new shares. The price per share moves to the old price divided by X. Total value held by each shareholder stays unchanged.

Walk through Nvidia's 2024 split. Before the split: roughly 2.5 billion shares trading at $1,200, a market cap of $3 trillion. After the 10-for-1: roughly 25 billion shares at $120, a market cap of $3 trillion. An investor holding 10 shares worth $12,000 ended up with 100 shares worth $12,000.

A reverse split runs the math in the other direction. The ratio is "1-for-X," so X old shares consolidate into 1 new share, and the price multiplies by X. A struggling company with 100 million shares at $0.50 could do a 1-for-10 reverse, leaving 10 million shares at $5. The market cap of $50 million would not move.

The trigger for a reverse split is usually compliance. Major exchanges delist stocks that trade below $1 for an extended period, so reverse splits restore the listing. They create no value, which is why the share price often drifts back down within months. ETFs also use reverse splits to keep the price of leveraged products in a manageable range.

Splits also adjust options contracts, share buybacks already in flight, and per-share targets in equity compensation plans. The point is to keep economic exposure flat across the change. Charts adjust historical prices for splits, which is why Apple's 1980 IPO price shows as roughly $0.10 in modern charts even though AAPL traded at $22 on day one.

Stock Split Scenarios Compared

Each split type sends a different signal about the company behind it.

| Dimension | Common Forward (2-for-1) | Big Forward (10-for-1) | Reverse Split (1-for-10) | Stock Dividend (10%) |

|---|---|---|---|---|

| Share count | Doubles | Multiplied by 10 | Cut to 10% of prior | Up by 10% |

| Price effect | Halves | Divided by 10 | Multiplied by 10 | Down by about 9% |

| Typical trigger | Stock at 100 to 300 USD | Stock above 500 USD | Sub-dollar listing risk | Tax-friendly distribution |

| Signal sent | Management confidence | Retail momentum, index access | Distress or exchange compliance | Capital preserved at company |

| Best for | Long-term holders | Index-tracked accounts | Avoiding delisting | Tax-deferred income |

The first two columns describe healthy companies advertising strength. The third is mostly companies in trouble, with a smaller group of mechanical reverse splits in ETFs and share-class cleanups (Citigroup did a 1-for-10 reverse split in 2011 from about $4.50 to $45 to absorb post-crisis dilution). A stock dividend issues paper instead of cash, popular with mature payers in some European markets and with US firms that want to reward holders without triggering a taxable cash event.

Where Stock Splits Mislead

The clean math hides three traps.

Splits do not create value. A 4-for-1 split that takes a stock from $400 to $100 has not made shareholders 75% richer. Each holder still owns the same fraction of the company, and the chart's "drop" on the ex-split date is not a discount.

Reverse splits are not always doom. Most are, since they fix delisting risk. But ETF issuers reverse-split routinely to keep contract sizes manageable, and a few mature companies have done reverse splits for share-class cleanups without trading lower afterward. Read the corporate action notice before reacting.

The split rally is partly mechanical. When a high-priced stock splits, retail buyers and option traders pile in around the announcement because the round-lot price drops. The buying tends to fade within a quarter, leaving the post-split chart flat or slightly down even when the underlying business stays strong.

The other thing splits affect is per-share metrics. After a 10-for-1 forward, earnings per share and dividends per share both drop by 90%, while the P/E ratio holds because the price drops 90% too. Comparing pre- and post-split per-share numbers without adjusting is one of the easiest mistakes a beginner makes. Index providers also rebalance weights on the ex-date, which can briefly move the free float figures used to size index allocations.

A stock split is a packaging change. The chart looks new, the broker statement shows more shares, and the price drop on the day of the split is not a price drop at all. What moves the price afterward is what the business does next.

Frequently Asked Questions

Do stock splits change the value of my investment? No. A split changes the number of shares you own and the price per share in opposite directions, so the total value of your position stays the same the second after the split as it was the second before. The underlying business and your ownership stake are unchanged.

What is the difference between a forward split and a reverse split? A forward split increases share count and reduces price (1 share becomes X shares at the price divided by X). A reverse split does the opposite, consolidating X shares into 1 at X times the price. Forward splits usually follow strong stock performance; reverse splits usually fix delisting risk.

Should I buy a stock before its split announcement? The split itself does not create value, so timing the announcement is not a reliable strategy. Studies show splitting companies have historically outperformed the market over the following year, but that reflects the strength of the underlying business, not the split. Buy on fundamentals, not the split mechanic.

Are stock splits taxable in the United States? Standard forward and reverse splits are not taxable events. Your cost basis is reallocated across the new share count, leaving the total basis unchanged. A stock dividend is also generally tax-free if it is pro-rata and does not change shareholder rights, though the rules vary by jurisdiction.