Updated

• 10 min read (EN)

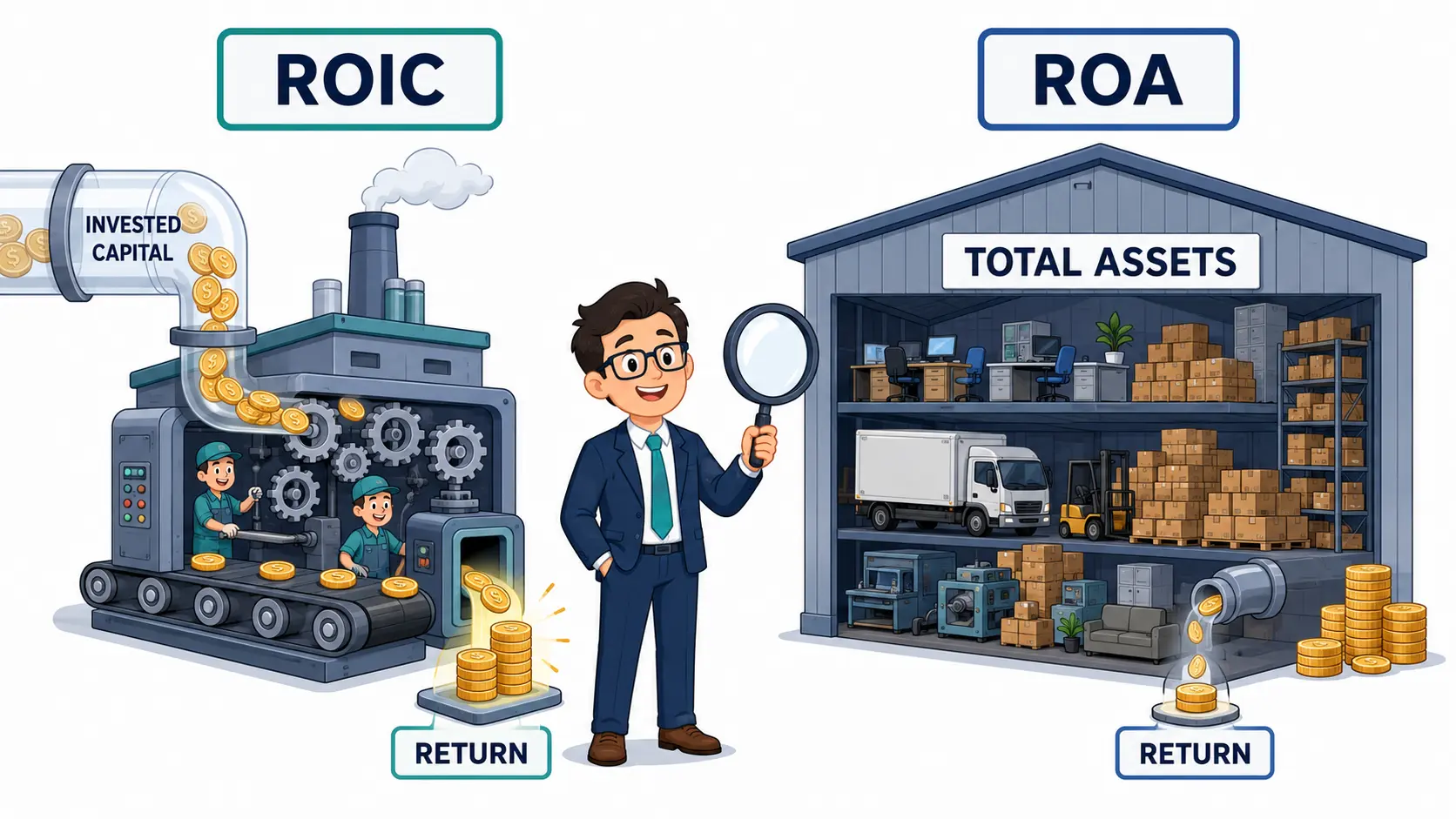

ROIC vs ROA: Capital Deployed vs Assets Held

ROIC measures return on the capital deployed in operations: NOPAT over debt plus equity minus excess cash. ROA measures return on every asset on the balance sheet: net income over total assets. The same business can post 15% ROIC and 10% ROA without changing operations, just by holding more cash or more debt. Use the wacc calculator to check whether either return clears the cost of capital.

ROIC vs ROA at a Glance

The cleanest summary: ROIC isolates operating performance, ROA reflects the entire balance sheet.

| Dimension | ROIC | ROA |

|---|---|---|

| Measures | Return on capital deployed in operations | Return on every asset on the balance sheet |

| Numerator | NOPAT, EBIT × (1 - tax rate) | Net income, after interest and after tax |

| Denominator | Debt + Equity - Excess Cash | Total assets, cash and goodwill included |

| Leverage | Neutral; NOPAT sits before interest | Distorts; interest cuts net income |

| Quality bar | 3+ points above WACC | 1.0-1.5% for banks, 5%+ for industrials |

| Fails when | Operating capital hard to split (banks) | Heavy cash piles or goodwill distort it |

| Best for | Cross-sector quality and value-creation checks | Bank profitability, asset-heavy industries |

What ROIC Tells You

ROIC equals Net Operating Profit After Tax (NOPAT) divided by invested capital, where invested capital is total debt plus equity minus excess cash. NOPAT is operating income (EBIT) times one minus the tax rate, so interest expense drops out of the numerator and capital structure stops moving the ratio. The metric answers: "For every dollar of productive capital inside the business, how many cents of operating profit does it earn after tax?"

The spread between ROIC and the weighted average cost of capital (WACC) is the engine of value creation in the McKinsey framework. ROIC above WACC means each reinvested dollar earns more than it costs. ROIC below WACC means growth destroys value, no matter how fast the top line moves. A quality screen demands ROIC at least 3 points above WACC across a full cycle.

Limitation: ROIC is harder to compute than ROA. Operating leases, capitalized research and development, goodwill, and the definition of "excess" cash vary across data providers. Two screens for the same company can publish ROIC figures 3-5 points apart.

Example: Costco's ROIC sits near 26%. Capital deployed is small relative to revenue, and the warehouse model recycles inventory faster than the company pays suppliers. That capital efficiency is one reason Costco keeps appearing on lists like top 10 wide-moat stocks year after year.

What ROA Tells You

ROA equals net income divided by average total assets. DuPont breaks it into profit margin times asset turnover, splitting profitability into the two levers a business pulls. The denominator includes everything on the balance sheet: cash, inventory, fixed assets, goodwill, even non-operating items. The metric answers: "For every dollar the company holds in assets, how many cents of profit reach the shareholder line?"

ROA is the standard measure of bank profitability for a reason. Loans dominate a bank's asset base, leverage is structural, and ROA normalizes profit by the size of the loan book. A community bank with $500 million in assets and a money-center bank with $2 trillion compare cleanly on ROA where absolute earnings cannot. Healthy US banks land in the 1.0-1.5% range, with leaders above 1.3%.

Limitation: ROA is not leverage-neutral. Net income drops when interest expense rises, but total assets do not, so two firms with the same operations and different debt loads report different ROAs. Cash piles, acquired goodwill, and revalued assets shift the ratio further without operations changing.

Example: Apple's reported 2022 ROA sat near 28%, high for a company of its scale. ROIC the same year was closer to 52%. The 24-point gap is mostly cash and short-term investments inflating the asset base. The operating engine is unchanged.

When to Use ROIC vs ROA

Different business models reward different metrics.

| Scenario | Better metric | Why |

|---|---|---|

| Banks, insurers, asset managers | ROA | Leverage is structural; ROIC inputs cannot be cleanly separated |

| Tech, industrial, consumer, retail | ROIC | Strips capital-structure noise; comparable across peers |

| Companies with large cash piles | ROIC | Excess cash inflates ROA's denominator without earning operating returns |

| Cross-sector quality screens | ROIC vs WACC | Absolute ROIC varies by industry; the WACC spread normalizes |

| Capital-intensive (utilities, airlines) | ROIC | Low ROA is expected; only the ROIC-WACC spread separates winners |

| Quick screen from headline figures | ROA | Net income and total assets sit on page one; NOPAT requires adjustment |

| Cyclical companies | Both, 10-year | One-year figures swing with the cycle on either metric |

Use ROIC when: comparing across capital structures or industries, judging whether reinvested capital creates value, or screening for moats.

Use ROA when: the business is a bank or insurer, or you need a number that fits on the back of an envelope.

Use both when: you want to see how cash, leverage, and operations interact. Watching the two together over a decade catches accounting noise a single metric misses.

Using ROIC and ROA Together

Calculate both and watch the gap. Within 3 percentage points means cash and leverage are not distorting the picture. A spread of 10 points or more tells a story: heavy cash, aggressive leverage, or goodwill from acquisitions. Good or warning, the gap deserves a second look.

A worked example: two businesses, identical operations. Both produce $200 million of operating income, face a 25% tax rate, and deploy $1,000 million of operating capital. Co A is all equity, no excess cash. Co B carries $800 million of debt at 5% interest and $200 million of idle cash, putting total assets at $1,200 million. NOPAT is $150 million in each case, so ROIC is 15% for both. Interest cuts Co B's net income to $120 million, and the larger asset base drags ROA to 10%. Same operations, 5-point gap.

For the equity slice, pair both with the ROE vs ROIC comparison: ROE adds the leverage signal ROIC strips out. The deciding number is rarely ROA or ROIC alone. It is the spread between ROIC and WACC. The broader set of paired metric breakdowns walks through valuation, cash, and earnings pairings in the same format. Open the wacc calculator for any stock to compute the cost of capital that turns either return into a usable signal.

Frequently Asked Questions

Why is ROIC usually higher than ROA? ROIC strips excess cash and non-interest-bearing liabilities out of the denominator and uses NOPAT in the numerator, which sits above interest expense. ROA divides net income by every asset on the balance sheet. For most companies that hold any cash or carry any debt, ROIC ends up larger than ROA on the same operating performance.

Why do banks use ROA instead of ROIC? A bank's assets are its loans, and its capital structure is dominated by deposits and other funding. Separating operating from financing capital is close to impossible, so the inputs ROIC requires become unreliable. ROA normalizes net income by the loan book and compares cleanly across institutions of very different sizes.

What ROIC level marks a high-quality business? A common quality screen requires ROIC sustained above 12-15% across a full cycle. Elite businesses keep ROIC above 20%. The more important test is the spread above WACC: ROIC at least 3 percentage points above the cost of capital signals genuine value creation. Anything below WACC destroys shareholder value no matter how high the absolute ROIC looks.

Why does a cash-rich company show low ROA and high ROIC? Cash sits in the ROA denominator but earns almost nothing in operating terms, dragging the ratio down. ROIC subtracts excess cash from the denominator before dividing, so the cash drag disappears. A company with $50 billion in idle cash on a $200 billion asset base looks mediocre on ROA and exceptional on ROIC, even though the operating business is unchanged.